SMM News on July 11:

As the first half of 2025 has passed, fluctuations in lead prices have had a profound impact on upstream and downstream industries. Under the combined influence of the macroeconomic environment, supply-demand relationship, and policy factors, the trend of lead prices has exhibited complex and volatile characteristics. This article will provide a comprehensive review of lead price trends in the first half of the year and conduct an in-depth analysis and outlook for the second half based on the current market situation.

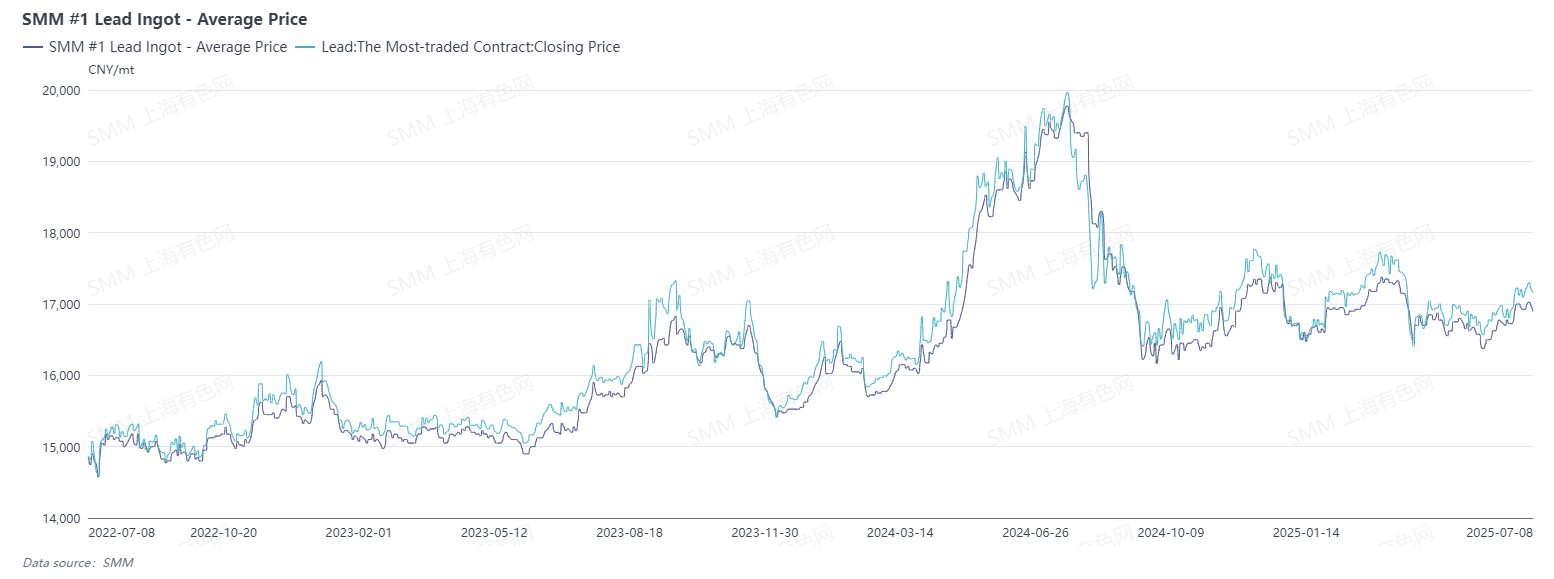

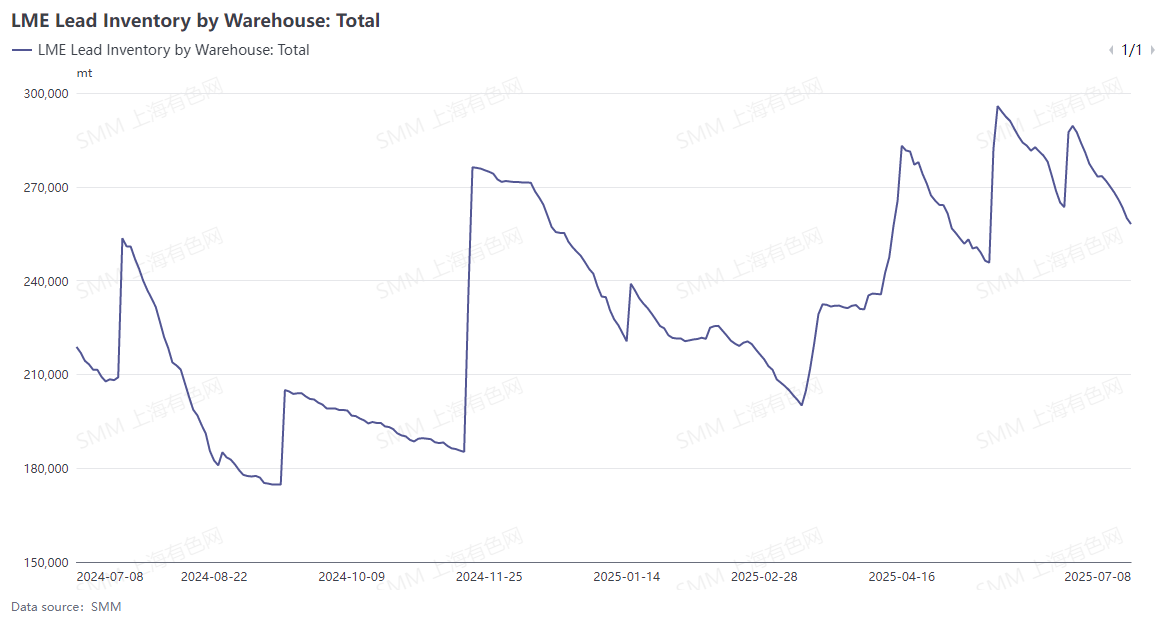

In January, lead prices showed a trend of initial decline followed by a rebound, with the overall operating range narrowing compared to December 2024. The fluctuation range of the most-traded SHFE lead contract was only around 600 yuan/mt, while the fluctuation range in the previous month exceeded 1,000 yuan/mt. As the Chinese New Year holiday approached, lead-acid battery enterprises gradually arranged for year-end inventory preparation and holiday schedules. From the perspective of end-use consumption, the market demand for lead-acid batteries was weak, and downstream enterprises were not actively preparing for inventory before the holiday. Purchases by large enterprises were relatively scattered, and they observed the market for a longer period. Especially after mid-January, spot premiums dropped rapidly, which contrasted with the resistance to decline shown by SHFE lead. The trend of lead prices in overseas markets was similar to that in the domestic market. LME lead prices fluctuated within a range throughout the month. Except for a single-day surge of nearly 20,000 mt in LME lead inventory in early January, destocking continued in the middle and late months, resulting in a monthly decrease of over 20,000 mt.

In February, as the Chinese New Year holiday ended in the Chinese market, enterprises in the upstream and downstream of the lead industry chain resumed production after the holiday, and transactions in the spot market gradually recovered. On the first trading day after the holiday, SHFE lead prices started on a positive note, with the most-traded contract climbing from 16,700 yuan/mt before the holiday to above 17,000 yuan/mt. Meanwhile, the US imposed a tariff hike, and the fundamental supply-demand situation remained stalemated. Domestic end-use consumption after the holiday fell short of expectations, and producers were not enthusiastic about resuming production, mostly operating in a produce-based-on-sales mode. The demand for lead ingot purchases also improved limitedly. Transactions in the lead spot market throughout the month were sluggish, and lead prices fluctuated at highs during the month. In overseas markets, although lead ingots were in a destocking state, there was also strong concern about the US tariff hike, and LME lead prices also fluctuated at highs.

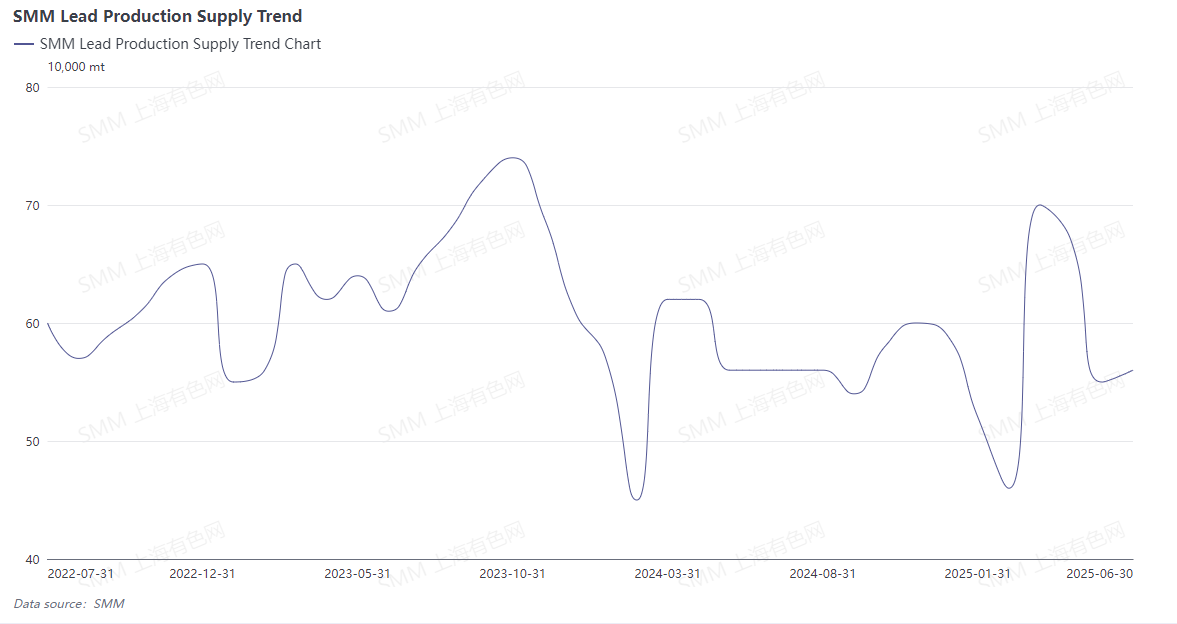

In March, after the US Fed's interest rate-setting meeting, the US dollar index continued to decline. Coupled with the downward trend in long-term contract negotiations for lead-zinc ores, both LME lead and zinc prices strengthened, with LME lead reaching a high of $2,104.5/mt. The "Two Sessions" were held in China, and many policies and measures were proposed to boost the economy, alleviating market concerns about the US tariff hike. Non-ferrous metals on the SHFE generally turned positive, with SHFE lead prices holding up well and reaching a high of 17,805 yuan/mt during the month, the highest in nearly three months. As the impact of the Chinese New Year holiday faded, primary lead and secondary lead smelters resumed production in a concentrated manner. Coupled with the commissioning of new secondary lead capacity, the monthly increase in lead ingot supply exceeded 50%. Additionally, the lead ingot import window briefly opened, bringing in some imported crude lead, and the monthly lead supply reached a one-and-a-half-year high. In late March, expectations of US tariff hikes intensified, and the traditional off-season expectations for the lead consumer market rose, causing lead prices to reverse and pull back, almost erasing all gains since March.

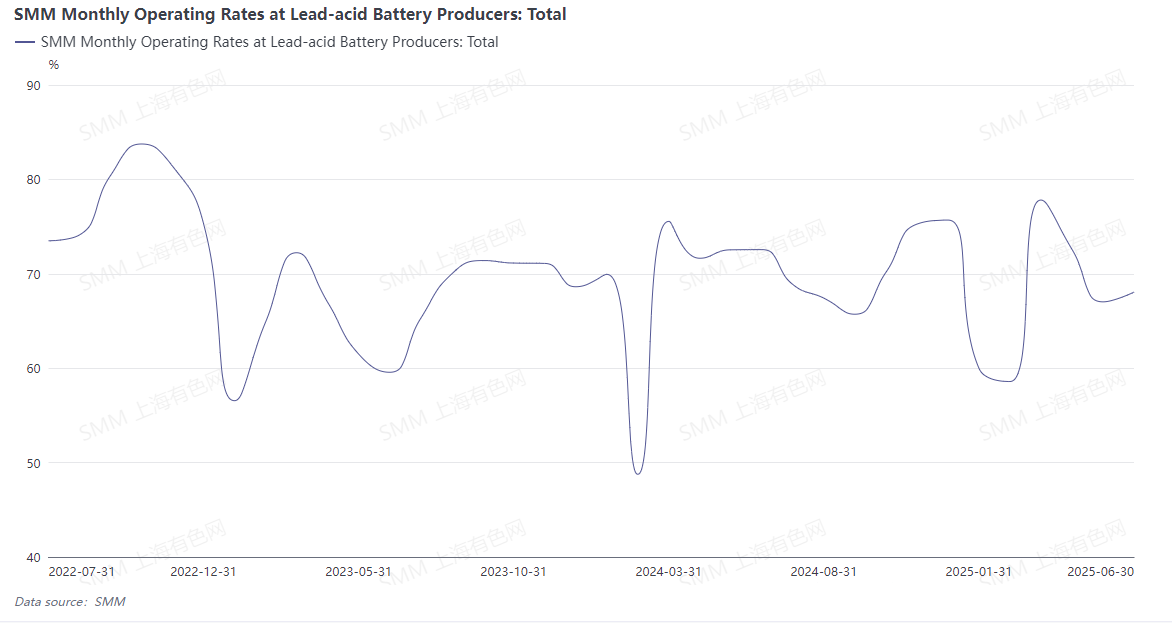

Early in April, the US implemented its "reciprocal tariff" policy, with escalating tariffs on China, covering commodities such as non-ferrous metals, automobiles, chips, soybeans, etc.. The US tariff policy triggered market volatility. Gold, as a major safe-haven asset, saw its price continue to soar. The most-traded SHFE gold futures contract surged to 836.3 yuan/gram, setting a new historical high once again. Meanwhile, non-ferrous metals generally fell under the tariff impact. LME lead prices declined continuously from the end of March until April 9, recording ten consecutive days of losses, with the lowest price reaching $1,837.5/mt, a new low since September 29, 2022. As the domestic lead-acid battery market entered the traditional off-season in April, lead-acid battery enterprises gradually reduced production or took holidays, weakening demand for lead. SHFE lead prices rapidly fell below the 17,000 yuan/mt threshold in early April, reaching a low of 16,165 yuan/mt, a new low since March 28, 2024. In mid-to-late April, lead prices mainly exhibited a corrective trend. Domestic secondary lead cost support played a role, coupled with increased demand from downstream enterprises building inventories at low prices, causing lead prices to gradually rebound to around the 17,000 yuan/mt level.

Following the US's announcement of "reciprocal tariffs" in April, China and the US held their first dialogue in early May, cancelling 91% of tariffs and suspending the implementation of 24% of tariffs. At the same time, the People's Bank of China announced RRR cuts and interest rate cuts. Despite the release of these two favourable macro front news, lead prices did not show a significant upward trend. Instead, they were dragged down by fundamental factors, with lead prices consolidating mainly between 16,500-17,000 yuan/mt throughout the month. As the off-season in the lead-acid battery market intensified in May, lead-acid battery enterprises further increased production cuts. Coupled with the Labour Day holiday, a few enterprises took holidays for up to half a month, significantly reducing lead consumption. Even against the backdrop of reduced lead ingot supply, lead ingot inventory buildup still occurred. Although overseas markets showed a trend of bottoming out and rebounding in early May due to the easing of tariff impacts, overseas LME lead inventory increased by over 20,000 mt in May, constraining the upside potential of lead prices. Lead prices repeatedly stalled at the $2,000/mt threshold.

In early June, the US "reciprocal tariff" issue resurfaced, escalating tariff risks and causing non-ferrous metals to generally weaken. Lead prices also entered a period of doldrums, with the most-traded SHFE lead contract once approaching the 16,500 yuan/mt threshold. The impact of the off-season in the lead-acid battery market in June had not yet subsided, and most producers adopted a produce-based-on-sales strategy. Additionally, as it was the mid-year period, a small number of enterprises sought to increase production and meet annual targets. In the first ten days of the month, spot lead prices fell below 16,500 yuan/mt, prompting downstream enterprises to gradually stock up on demand. Lead ingots were transferred from smelter in-plant inventories to downstream enterprise in-plant inventories, leading to an improvement in apparent consumption. After mid-to-late June, domestic lead smelters increased maintenance, coupled with environmental protection inspections, causing secondary lead enterprises to delay production resumptions. Primary lead inventories were gradually depleted, leading lead prices to stop falling and rebound, breaking through the 17,000 yuan/mt threshold near month-end. The most-traded SHFE lead contract reached a high of 17,270 yuan/mt, setting a new three-month high.

Entering July, lead prices continued to hold up well, with the interaction between tight raw material supply and expectations for the peak consumption season driving the overall center of LME lead and SHFE lead prices higher, with the most-traded SHFE lead contract reaching a high of 17,315 yuan/mt at the beginning of the month. The expected increase in lead ingot supply in July was due to the resumption of production after maintenance, the lifting of environmental protection factors, and the commissioning of new capacity.The lead-acid battery market entered a transition period from the off-season to the peak season, with some enterprises showing relatively improved production enthusiasm. Considering the traditional practice of stocking up before the peak season, it is expected that lead-acid battery enterprise production will steadily increase in July, bringing corresponding consumption growth. It is worth noting that the limitations of raw material supply may constrain the increase in lead ingots, and the lack of improvement in terminal consumption in the lead-acid battery market may also limit the improvement in production enthusiasm among downstream enterprises.

Macro side,US President Trump stated that reciprocal tariffs would be implemented starting August 1 and would not be postponed again, warning that tax letters to the EU were forthcoming.Trump threatened to impose a 50% tariff on copper and a 200% tariff on pharmaceuticals, with the nearest-month contract for New York copper seeing its largest increase since 1968. Multiple countries responded to Trump's tariffs: Japan and South Korea sought to continue negotiations, South Africa argued that tariffs could still be reduced, and Brazil condemned and emphasized retaliation. The US Treasury Secretary spoke with Japan's chief negotiator by phone and was rumored to visit Japan next week. Germany warned that the EU was prepared to retaliate if a fair trade agreement could not be reached. Trump expressed "great dissatisfaction" with Putin and threatened additional sanctions against Russia. Additionally, the US Fed: The US one-year inflation expectation in June fell to a five-month low, with concerns about layoffs easing.Although August-September is the traditional peak consumption season for lead-acid batteries, and bullish sentiment is high, the impact of the US "reciprocal tariff" issue poses significant uncertainty, necessitating vigilance against the risk of lead prices jumping initially and then pulling back.

Additionally, due to the impact of tariffs and the decline in overseas lead and zinc mine supply, the supplementary role of imported lead concentrates in the domestic market will be relatively limited in the second half of the year (H2). After the National Day holiday, as the traditional "winter stockpiling" season approaches, the high demand for lead concentrates from domestic smelters may lead to a continued decline in their processing charges (TCs). At that time, the demand for waste lead-acid batteries, which serve as a supplementary raw material for some primary lead smelters, will also increase. Given the overcapacity in secondary lead production and the existing undersupply of waste lead-acid batteries, SMM expects that the price of scrap batteries will remain more likely to rise than fall in H2, leading to increased competitive pressure among enterprises.

As the weather cools, the consumption of mainstream lead-acid batteries will weaken, with operating rates declining at leading producers and a reduced willingness to purchase lead ingots. Bearish sentiment will begin to dominate the market. Due to the high prices of scrap batteries, secondary lead smelters may enter a concentrated maintenance season again due to loss pressures, advancing into the New Year's Day and Chinese New Year holidays. Except for some primary lead smelters that have annual maintenance expectations, other enterprises are expected to maintain stable production. According to past experience, the demand for overseas purchases of lead-acid batteries rises before Christmas; however, due to the impact of tariff events, China's battery export orders may decline significantly YoY compared to previous years. At that time, there is a high probability that the lead price trend will show overseas market outperforming domestic market.

In summary, it is difficult to change the pattern of high domestic raw material prices in H2, and the lead price trend may rise first and then decline.